Understanding SEC Pay Versus Performance (PvP) Reporting Requirements

Executive compensation has long been a point of focus for investors, regulators, and corporate governance professionals. In recent years, the U.S. Securities and Exchange Commission (SEC) has increased transparency requirements surrounding how executive pay aligns with company performance. The most significant development in this area is the SEC’s Pay Versus Performance (PvP) disclosure rule.

Background on SEC Pay Versus Performance Rules

On August 25, 2022, the SEC adopted final rules implementing the Pay Versus Performance disclosure requirements mandated under the Dodd-Frank Wall Street Reform and Consumer Protection Act. The rules require public companies to disclose the relationship between executive compensation actually paid to named executive officers (NEOs) and the company’s financial performance.

The purpose of the rule is to increase transparency for investors by allowing them to compare executive compensation outcomes against measurable company performance metrics over time.

The SEC’s final rules require companies to include PvP disclosures in proxy statements or information statements that contain executive compensation disclosures.

The disclosures focus on several key areas, including:

- Total compensation of the CEO

- Average total compensation of other named executive officers

- Compensation “actually paid” to the CEO

- Average compensation “actually paid” to other NEOs

- Company cumulative total shareholder return (TSR)

- Net income

- A company-selected financial performance measure deemed most important in linking executive compensation to performance

Companies may also voluntarily include supplemental financial performance measures if they believe additional context would be useful for investors.

Which Companies Are Required to Report?

The SEC’s Pay Versus Performance disclosure rules generally apply to all public companies that are required to provide executive compensation disclosures under SEC rules.

However, there are important distinctions and exemptions.

Companies Required to Comply

The following issuers are generally required to provide PvP disclosures:

- Domestic public companies

- Large accelerated filers

- Accelerated filers

- Non-accelerated filers

- Smaller reporting companies (with scaled disclosure accommodations)

Companies with Modified Requirements

Smaller Reporting Companies (SRCs)

Smaller reporting companies may provide disclosures for only three fiscal years rather than five. SRCs are also not required to include peer group TSR or a company-selected measure.

Newly Public Companies

Newly public companies are not expected to immediately provide five years of historical disclosure. Instead, they may phase in disclosures over time as additional fiscal years become available.

Exempt Companies

The following issuers are exempt from the Pay Versus Performance disclosure requirements:

- Emerging growth companies (EGCs)

- Foreign private issuers (FPIs)

- Registered investment companies

Required Time Period for Reporting

Most public companies must disclose Pay Versus Performance information covering the five most recently completed fiscal years.

However, companies are allowed to phase in the disclosures during the initial years of compliance.

The phase-in generally works as follows:

- Year 1 filing: provide 3 fiscal years

- Year 2 filing: provide 4 fiscal years

- Year 3 filing and beyond: provide full 5 fiscal years

Smaller reporting companies may permanently provide only three years of disclosure instead of five.

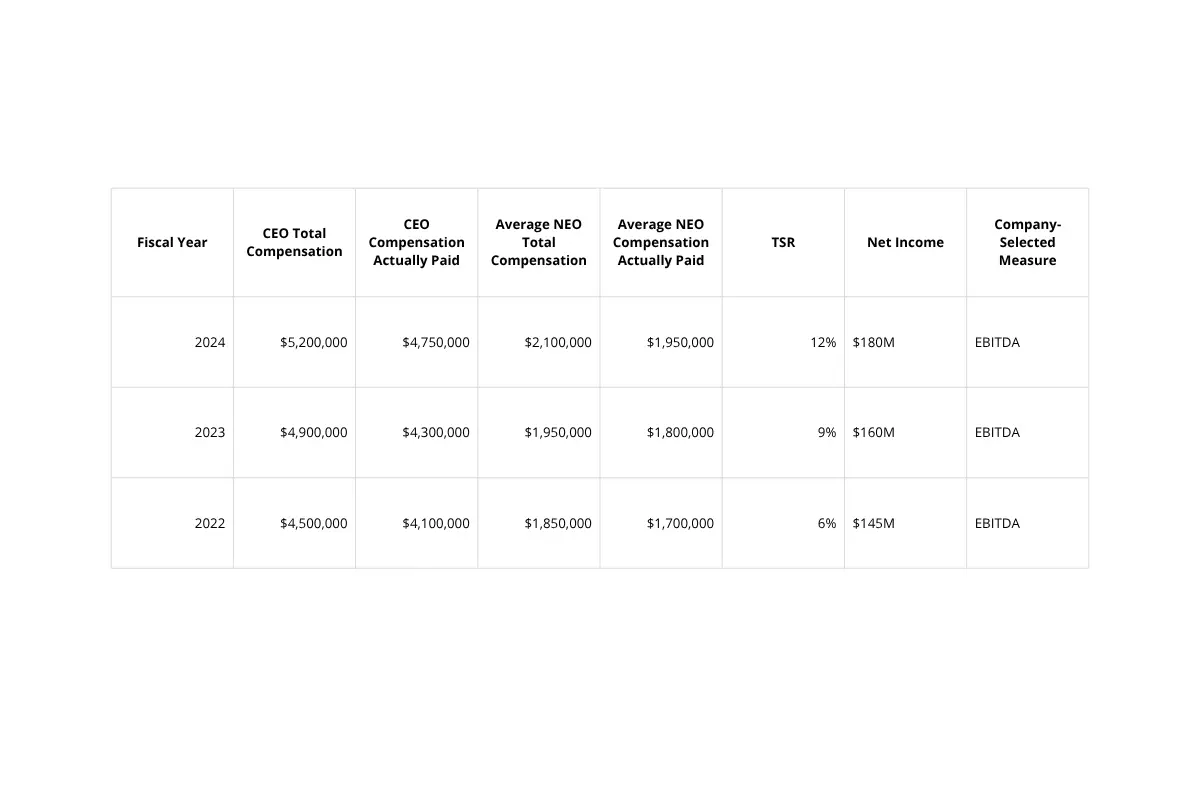

What Must Be Included in the PvP Table?

At the center of the SEC’s requirements is the Pay Versus Performance table. This table presents compensation and financial performance data in a standardized format.

An example PvP table looks like this:

In addition to the table itself, companies must provide:

- A clear description of the relationship between compensation actually paid and company performance

- Narrative or graphical explanations comparing compensation and financial metrics

- Footnote disclosures showing adjustments used to calculate compensation actually paid

Best Practices for Staying Compliant

Complying with SEC Pay Versus Performance requirements can be complex, particularly for companies with sophisticated equity compensation structures. The following best practices can help organizations maintain compliance and improve reporting accuracy.

Establish cross-functional coordination between legal, finance, HR, and external advisors

- Maintain detailed valuation documentation

- Review equity compensation processes to evaluate valuation methods

- Conduct early draft reviews to identify inconsistencies, validate calculations, and resolve ongoing concerns

- Review peer company’s PvP filings to understand emerging disclosure practices

- Monitor SEC guidances to avoid reporting deficiencies

Final Thoughts

The SEC’s Pay Versus Performance rules represent a major step toward greater executive compensation transparency. By requiring companies to directly compare executive pay with measurable company performance, the SEC aims to provide investors with clearer insight into corporate pay practices.

Although the reporting requirements can be technical and calculation-intensive, organizations that establish strong internal controls and proactive disclosure processes can effectively manage compliance obligations.

As investors continue to focus on executive accountability and governance transparency, Pay Versus Performance reporting will likely remain a critical component of public company disclosures for years to come.

Interested in learning about pay transparency? Check out our upcoming webinar. Register here!